Here’s the full story — and everything you actually need to know about Germany crypto tax in 2026 before the Finanzamt comes knocking.

■ LEGAL DISCLAIMER

This article is based on personal experience and publicly available information about German tax law as

of May 2026. It is not legal or financial advice. German crypto tax rules change frequently. Always consult

a qualified Steuerberater (tax advisor) specialising in cryptocurrency before making decisions about your

holdings or filing your tax return.

My €47,000 Mistake — and Why It Happened

It was a Tuesday afternoon in Frankfurt. I remember the light coming through the window at an odd angle, the kind that makes you squint when you’d rather be anywhere else. The accountant’s desk was immaculate. My records were not.

I sat there explaining my crypto positions — Bitcoin I’d bought in 2019, a handful of Ethereum

trades from 2020, staking rewards I’d received and, honestly, mostly forgotten about. He kept

nodding. Kept saying ‘ja, ja.’ I thought that was a good sign.

It was not. He was just being German-accountant polite. His pen kept moving, and the number at the bottom of his notepad kept climbing.

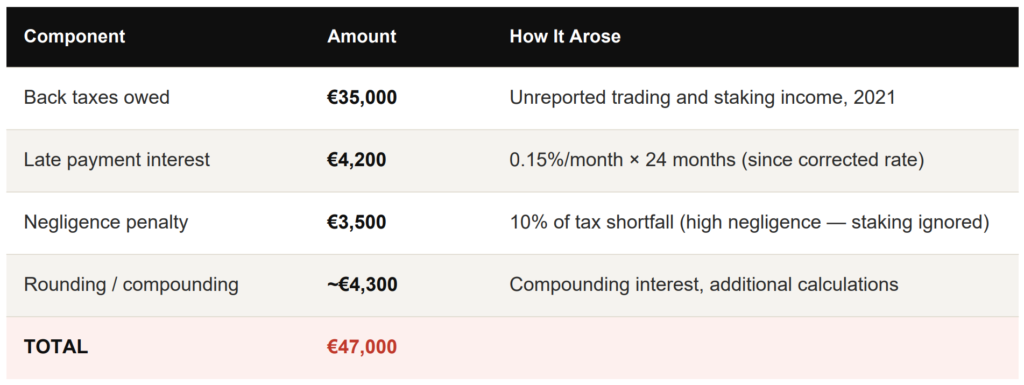

€47,000. Back taxes, interest and penalties. For activity I’d done three years earlier and assumed was either fine or irrelevant.

I wasn’t trying to dodge anything. I genuinely didn’t understand how German crypto tax worked. I’d read in some Discord server that Germany was ‘crypto-friendly.’ Someone said something about a one-year rule. I took that to mean if I held for a year, I was in the clear, full stop. I was wrong — but not in the way you’d expect.

“Ignorance, in the German tax system, is not a defense. It is just more expensive.”

The part that genuinely surprised me wasn’t the tax itself — it was how comprehensively the

Finanzamt already knew about my activity. They had data from exchanges. They had blockchain

records. They weren’t guessing. They were just waiting for me to file correctly, and when I didn’t,

they came to me.

German crypto audits jumped 340% between 2022 and 2024. The Finanzamt has exchange

partnerships, on-chain analytics tools, and the legal authority to go back ten years. If you’ve been

treating crypto tax as optional, this article is for you.

2. How Germany Crypto Tax System Actually Works

Most people hear ‘Germany crypto tax’ and think there’s one rule that covers everything. There

isn’t. Germany categorises crypto income into distinct buckets, and each one is taxed differently.

Getting the bucket wrong is exactly how people end up in a Frankfurt office having a bad Tuesday.

The Three Tax Categories

1 — Sonstige Einkünfte / Spekulationsgewinne (Speculative Gains)

This is where most crypto activity lands. Under §23 EStG (Einkommensteuergesetz), private sales

of assets — including cryptocurrency — within a one-year holding period are taxed as ‘other

income’ (sonstige Einkünfte) at your personal income tax rate. This is your marginal rate, which can

go up to 45% for high earners.

Every trade, every sell, every token swap is a separate taxable event in this bucket. Most retail

traders live here without realising it.

2 — Long-Term Capital Gains (Over One Year)

If you hold cryptocurrency for more than one year and then sell, that gain is completely tax-free

under §23 Abs. 1 Nr. 2 EStG. No cap on the amount. No special threshold. Zero tax, regardless of

whether you made €1,000 or €1,000,000.

✓ KEY FACT — TAX-FREE AFTER ONE YEAR

Cryptocurrency held for more than 12 months and then sold is 100% tax-free in Germany with no upper

limit on gains. This applies to Bitcoin, Ethereum and most other cryptocurrencies held as private assets.

This is confirmed under §23 Abs. 1 Nr. 2 EStG and has been the law since the Bundesfinanzministerium

first clarified crypto’s treatment.

3 — Einkünfte aus Gewerbebetrieb (Business Income)

If the Finanzamt decides you’re running a crypto trading business rather than simply investing, your

income shifts into the business category. This means trade tax (Gewerbesteuer) applies, you may

need to register a business, and losses carry forward differently. The threshold isn’t perfectly

defined in law, but making 10 or more trades per month will draw scrutiny.

How the Finanzamt Decides: Trader vs. Investor

This distinction matters more than people realise. The Finanzamt looks at frequency, volume, and

stated intention. There’s no hard rule — it’s assessed case by case. But as a rough guide: a few

trades per month with a long-term view keeps you in the investor category. Daily or high-frequency

trading for income pushes you toward the business category, with all the complexity that brings.

3. The One-Year Holding Period Rule — Corrected and

Explained

This is the rule that, understood correctly, makes Germany genuinely one of the better places in

Europe for long-term crypto investors. But it’s also the rule that causes the most confusion —

because it’s regularly misquoted online.

■ CORRECTING A COMMON MYTH

Many articles, forums and even some advisors claim that Germany’s tax-free crypto rule only applies if

your gains are below €600. This is wrong. The €600 Freigrenze (explained in the next section) applies to

SHORT-TERM gains — crypto held for less than one year. Long-term gains (held over one year) are

completely tax-free with NO limit on the amount. These are two entirely separate rules.

The Core Rule, Stated Clearly

Under §23 EStG: if you buy cryptocurrency and sell it after holding for more than 12 months, the

entire gain is exempt from tax. That’s it. No forms to file for that gain, no threshold to stay under, no

special application required. The clock starts on the day of purchase and ends on the day of sale.

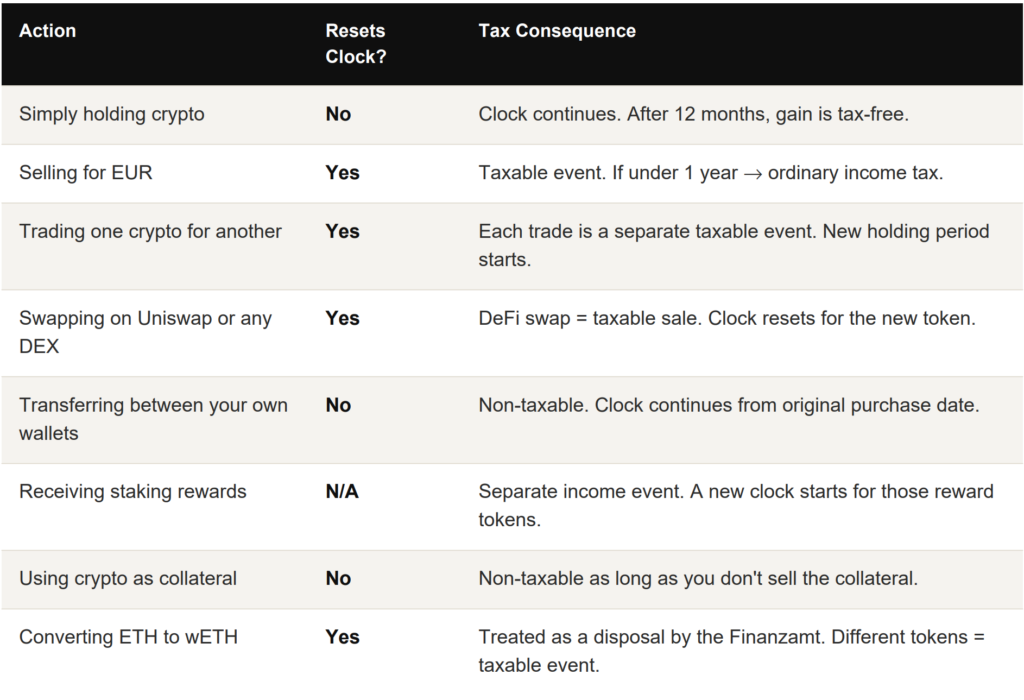

What Resets the Clock

The practical trap here is that the average German crypto trader — according to BaFin data —

makes around 4.3 trades per month. Every trade resets the clock for that portion of their holdings.

Most people are therefore stuck in the short-term speculative income bracket at their full marginal

rate, even if they thought of themselves as ‘investors.”

The one-year rule rewards patience and penalises impatience. If you can actually hold without

touching your position, Germany becomes one of the most tax-efficient jurisdictions in Europe for

crypto. If you trade frequently, it becomes one of the most expensive.

4. The €600 Freigrenze — What It Actually Means

This exemption gets misunderstood almost every time it’s mentioned. Let’s clear it up once and for

all.

Under §23 Abs. 3 Satz 5 EStG, there is an annual Freigrenze of €600 for private sale gains —

meaning gains from assets held less than one year. If your total short-term gains for the year are

below €600, you pay no tax on them at all.

■ FREIGRENZE VS. FREIBETRAG — AN IMPORTANT DISTINCTION

A Freigrenze is a threshold, not an allowance. If your short-term gains are €599, you pay zero tax. If they

are €601, you pay tax on the full €601 — not just the €1 above the threshold. This trips people up. The

€600 is not a deductible amount; it is a cliff edge. Cross it, and the whole amount becomes taxable.

What the €600 Freigrenze Does NOT Cover

The exemption only applies to speculative gains from assets held under one year. It does not apply

to staking income, mining income, DeFi yield, or any other form of crypto earnings. Those are

taxed as ordinary income from the first euro. This is a separate tax bucket entirely.

And to repeat: long-term gains (held over one year) don’t need the Freigrenze at all. They’re

already fully tax-free. The two rules operate independently.

5. German Staking Tax: The 2024 Ruling That Changed

Everything

For years, there was genuine ambiguity in Germany about how staking rewards should be treated.

Were they capital gains? Were they income? Could you argue they didn’t exist until you sold them?

In early 2024, the Bundesfinanzministerium settled the question definitively.

The Ruling: Taxable on Receipt, at Market Value

Staking rewards are treated as ordinary income (sonstige Einkünfte) in Germany. They become

taxable the moment they hit your wallet, valued in EUR at the market rate on that specific day. Not

when you sell them. Not when the market recovers. The day you receive them.

This has brutal implications for anyone staking through a bear market. Here’s the scenario that

broke a lot of strategies:

The Staking Tax Trap — A Real ScenarioTitle

January 2023: You stake 10 ETH (total value €20,000). Throughout 2023: You earn 0.5 ETH in staking

rewards. Average price during receipt: €2,500/ETH. Taxable income recognised: €1,250. April 2024: ETH

crashes to €1,500. Your 0.5 ETH reward is now worth €750. The problem: You owe income tax on €1,250

of ‘income’ that is now worth only €750. And you cannot offset staking income losses against trading

losses — they are in different tax buckets. If you sell the rewards to cover your tax bill, you may realise a

further capital loss — which also cannot offset the income tax already owed.

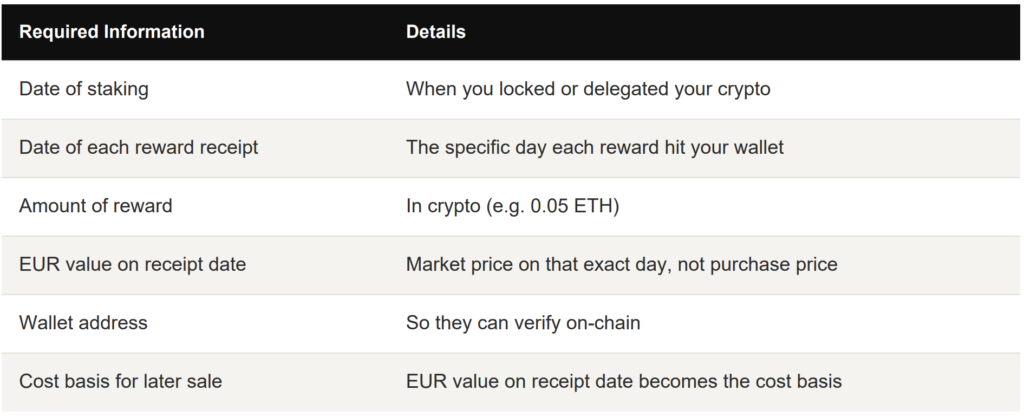

What the Finanzamt Needs for Staking Records

Most exchanges don’t format staking data in a way that satisfies the Finanzamt. Staking pools

rarely do either. This is where crypto tax software —

, Accointing, or CoinTracker —

becomes genuinely essential rather than just convenient. These tools pull your reward history and

calculate the EUR value on each receipt date automatically. (See our guide to the best crypto tax

software for Germany [internal link: /best-crypto-tax-software/] for a full comparison.)

6. Crypto Trading, Mining and DeFi — How Germany

Taxes Each

Trading

Every trade is a taxable event, whether it happens on a centralised exchange or a DEX. The key

variable is holding period. Under one year: you pay income tax at your marginal rate. Over one

year: tax-free.

Crypto-to-crypto trades are taxed the same as crypto-to-EUR trades. If you swap ETH for USDT on

Binance and both have been held for less than a year, you’ve realised a taxable gain or loss at that

moment. The fact that you never touched euros is irrelevant to the Finanzamt

FIFO (first in, first out) is the standard cost basis method used in Germany. This means the first

coins you bought are treated as the first ones sold. Some tax software allows other methods —

check with your Steuerberater about what the Finanzamt will accept for your specific situation.

Mining

Mining income is treated as ordinary income taxable on the day you receive the mined coins, at the

EUR value on that day. If you mine 0.05 BTC when Bitcoin is trading at €60,000, that’s €3,000 in

taxable income for that year.

The cost basis for mined coins is the EUR value at the time you received them. If you later sell

those coins, only the appreciation above that cost basis is taxable as a gain — and the one-year

rule applies from the day you mined them.

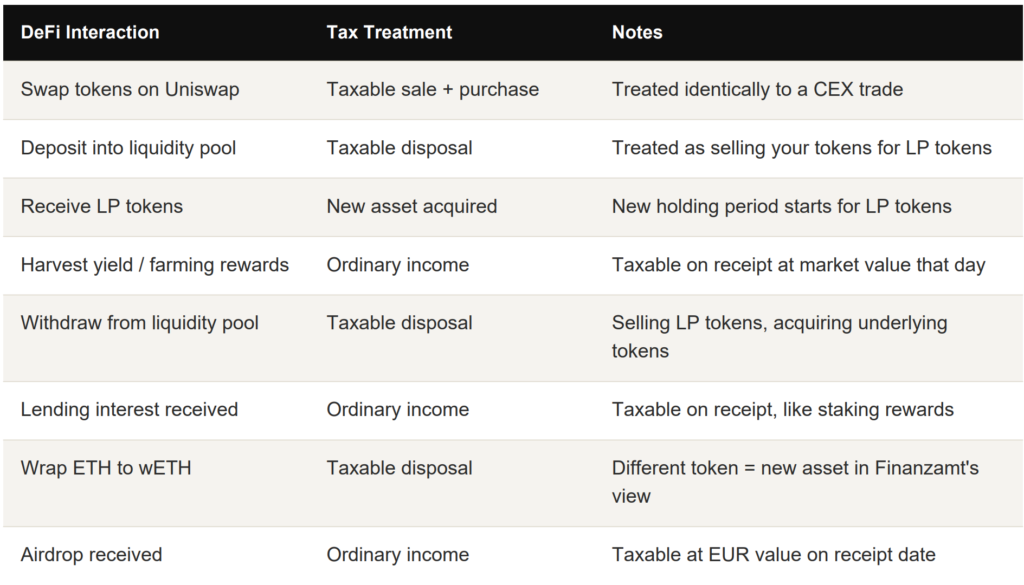

DeFi — The Area Most People Get Wrong

DeFi taxation in Germany is comprehensive and sometimes harsh. The Finanzamt has been clear:

DeFi is not a grey area. Here is how common DeFi interactions are treated:

The Finanzamt can and does trace DeFi transactions on-chain. You cannot hide activity by using a

DEX instead of a centralised exchange. If anything, on-chain activity is more transparent to

auditors because the blockchain is a permanent public record.

7. Record-Keeping: Your Biggest Risk Isn’t the Tax Rate

I used to think my problem was the tax rate. It wasn’t. My problem was that I couldn’t prove

anything. When the Finanzamt came, I had no documentation, no transaction logs, no exchange

statements — nothing organised. And without documentation, they switched to Schätzung:

estimation.

“The Finanzamt doesn’t want your best guess. It doesn’t want a

spreadsheet you built from memory. It wants precision that borders

on obsessive.”

What Schätzung (Estimation) Means for You

When you can’t produce records, the Finanzamt estimates your tax liability based on available data

— and they estimate against you. They looked at my Kraken deposits of €30,000 and assumed I’d

turned all of it into €47,000 in profit. Without documentation, I had no way to prove otherwise.

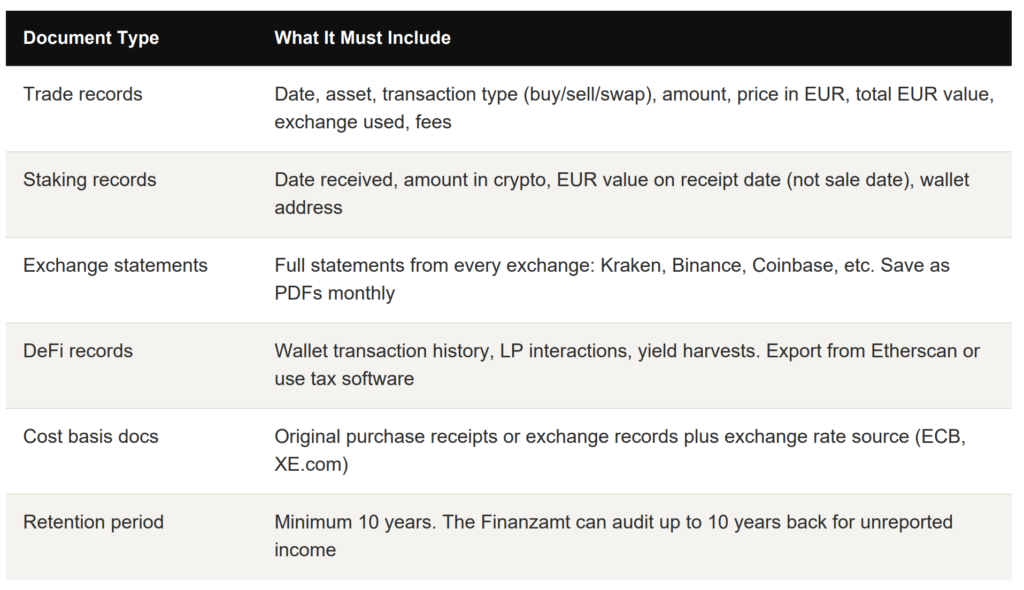

What to Keep — The Finanzamt’s Checklist

→ RECOMMENDED TOOLS

Koinly (koinly.io) — Automatic exchange imports, German tax report export. Supports DeFi and NFT activity.Accointing — Built specifically with German tax rules in mind. Handles staking reward valuation.

CoinTracker — Strong DeFi tracking, good for complex multi-chain portfolios. These tools cost €100–500

per year and generate formatted reports your Steuerberater can use directly.

8. The Finanzamt Audit Process — Step by Step

Getting audited for crypto in Germany follows a fairly predictable process. Here’s what actually

happens, based on direct experience.

Stage 1: The Letter

Aufforderung zur Abgabe einer Steuererklärung. A certified letter arrives requesting documentation

for your crypto holdings and transactions for the year in question. You have 30 days to respond.

You can request an extension — usually granted if you ask promptly and have a Steuerberater. Do

not ignore this letter.

Stage 2: Documentation Submission

You submit your records. If they’re comprehensive and credible, the Finanzamt may issue a

straightforward adjustment with minimal additional scrutiny. If documentation is incomplete or

missing, they move to estimation (Schätzung) mode. This is where having a crypto tax specialist

makes an immediate, measurable difference.

Stage 3: Assessment (Veranlagung)

The Finanzamt issues their calculation of your tax liability. You have one month to accept it or

appeal. Most people accept out of exhaustion. That’s often the wrong move — even a partially

correct assessment can be worth appealing, and a Steuerberater can identify errors.

Stage 4: Payment

Back taxes, interest and penalties become due. Payment plans (up to 60 months) are available if

you can’t pay in one go, but require a formal application. Interest continues to accrue during any

payment plan.

Can You Negotiate With the Finanzamt?

Yes, but almost only with professional help. A Steuerberater who specialises in crypto can argue

for reduced penalties (from 10% to 5% or lower), interest waivers in cases of genuine hardship,

and manageable payment plans. Without representation, you’re unlikely to get meaningful

concessions.

9. BaFin’s 2023 Crackdown and What Changed

BaFin — Germany’s financial regulator — doesn’t set tax policy, but their decisions have direct

consequences for how crypto is taxed and monitored. In 2023, they came down hard on crypto

exchanges operating in Germany.

Kraken pulled out of German derivatives trading. Binance began enforcing stricter KYC

requirements and tightened withdrawal limits for German accounts. Coinbase scaled back services

due to regulatory uncertainty. None of this made crypto illegal — it made crypto traceable.

BaFin regulations now require exchanges operating in Germany to maintain transaction records

and provide them to the Finanzamt on request. Your trades are not hidden. They’re documented,

timestamped, and accessible to tax authorities through formal data-sharing agreements.

If you didn’t report trades on Kraken or Binance between 2020 and 2024, the Finanzamt may

already have the data. They’re just waiting for your return to cross-reference it.

10. German Crypto Tax Rates by Income Type (2026)

Income Tax Brackets (Spekulationsgewinne / Staking / Mining / DeFi)

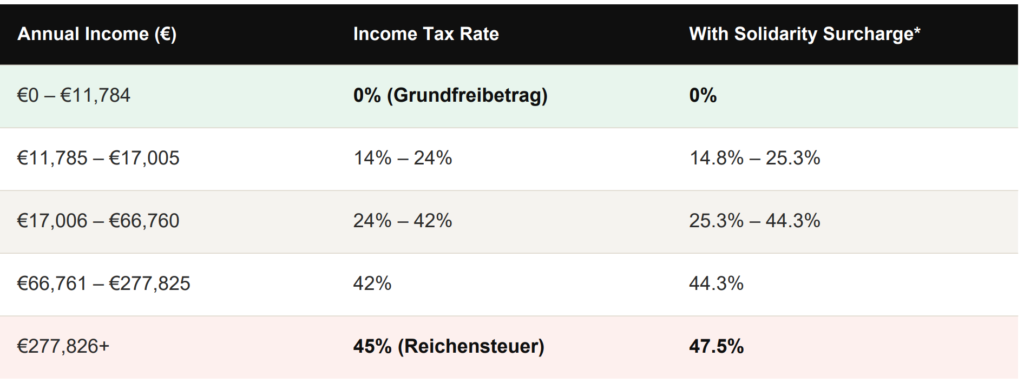

- The Solidarity Surcharge (Solidaritätszuschlag) was largely abolished from 2021 for the vast

majority of taxpayers. As of 2026, it only applies to individuals with a tax liability above the

exemption threshold (roughly €96,820 annual income for singles). If you’re a high earner paying

the top rate, add 5.5% on top of your income tax rate. If you’re a normal earner, you likely pay zero

Soli.

■ CHURCH TAX (KIRCHENSTEUER) — ONLY IF APPLICABLE

Church tax (8–9% of your income tax, depending on your German state) only applies if you are registered

as a member of a recognised church in Germany. It is not universal. If you have left the church

(Kirchenaustritt) or were never registered, you do not pay this. Factoring it into every calculation, as many

articles do, is misleading

Capital Gains (Over One Year) — Rate Summary

✓ LONG-TERM GAINS: COMPLETELY TAX-FREE

Cryptocurrency held for more than 12 months: 0% tax regardless of gain size. No Soli. No church tax. No

income tax. This is confirmed under §23 Abs. 1 Nr. 2 EStG and applies to private investors. This is the

single most important rule in German crypto taxation.

11. Penalties, Interest and Back Taxes — The Real

Numbers

Late Payment Interest

A correction from many older articles: Germany’s late payment interest rate for taxes was changed

by the Bundesverfassungsgericht (Federal Constitutional Court) in 2021, which ruled the old 0.5%

per month rate unconstitutional. Since 2022, the rate is 0.15% per month (1.8% per year). It still

compounds, but it’s no longer as extreme as older sources suggest.

Negligence Penalties

If you failed to report through carelessness rather than deliberate intent, the standard negligence

penalty (Fahrlässigkeit) is 5% of the tax shortfall. In cases of high negligence — where you

received income and made no effort to track or report it — this can climb to 10%.

Tax Evasion (Steuerhinterziehung)

Intentional evasion carries penalties of 50–100% of the tax shortfall and can result in criminal

prosecution. The distinction between negligence and evasion often comes down to whether you

received professional tax advice and ignored it. Most audit cases for crypto land in the negligence

category.

What My €47,000 Bill Actually Broke Down To

12. How to Calculate Your German Crypto Taxes —

Worked Example

Let’s walk through a realistic 2024 tax year to show exactly how this works in practice. This uses

the corrected rules — not the common misunderstanding.

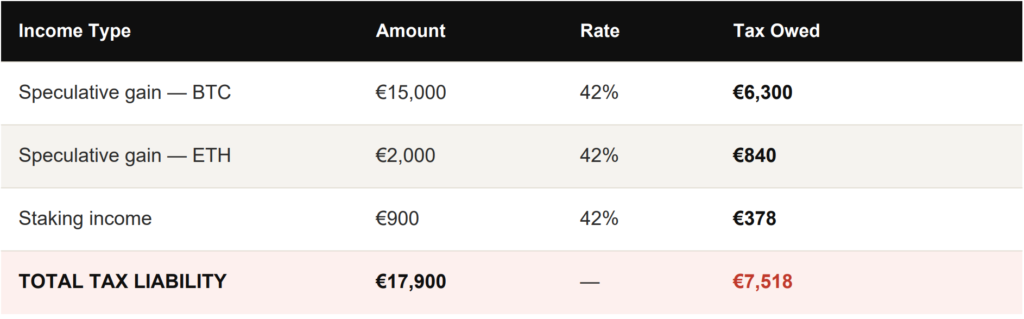

Scenario: Your 2024 Activity

- January: Buy 1 BTC for €50,000

- March: Stake 10 ETH (total value €30,000). Non-taxable event.

- May: Receive 0.3 ETH staking rewards when ETH is at €3,000. Value: €900.

- September: Sell 1 BTC for €65,000. Held 8 months (under 1 year).

- December: Sell 2 ETH from your original stake. Original cost: €6,000. Sale price: €8,000. Held 9+

months (under 1 year).

Step 1: Categories Each Transaction

| Transaction | Category | Holding Period |

|---|---|---|

| Buy 1 BTC | N/A (acquisition) | — |

| Stake 10 ETH | Non-taxable | Clock continues from purchase date |

| Receive 0.3 ETH reward | Ordinary income | Taxable on receipt. New holding period starts for reward ETH. |

| Sell 1 BTC | Speculative gain (§23 EStG) | 8 months — under 1 year → taxable |

| Sell 2 ETH | Speculative gain (§23 EStG) | 9+ months — under 1 year → taxable |

Step 2: Calculate Each Gain

BTC trade: Sell €65,000 − Buy €50,000 = €15,000 gain. Held under 1 year → speculative income.

Staking reward: 0.3 ETH × €3,000 = €900 ordinary income. Recognised in May when received.

ETH sale: Sell €8,000 − Buy €6,000 = €2,000 gain. Held under 1 year → speculative income.

Step 3: Apply the €600 Freigrenze

Total short-term speculative gains: €15,000 + €2,000 = €17,000. This exceeds €600, so the

Freigrenze does not apply. The full €17,000 is taxable.

Step 4: Calculate Tax (assuming 42% marginal rate, no Soli, no church tax)

→ HOW DIFFERENT WOULD IT HAVE BEEN?

If you had held the BTC for 4 more months (total 12+ months): €15,000 gain = €0 tax. The ETH held

another 3 months: €2,000 gain = €0 tax. Total tax saved: €7,140. The one-year rule is not a minor

technicality. It is the foundation of any tax-efficient crypto strategy in Germany. See our crypto tax

calculator [internal link: /crypto-tax-calculator/] to run your own numbers.

13. Finding a Crypto Tax Advisor in Germany

(Steuerberater)

If you’ve done anything beyond simply buying and holding — if you’ve staked, traded, used DeFi,

or moved coins between wallets — you need a Steuerberater who understands crypto. A regular

accountant will not be enough.

Why Most Regular Accountants Fail at Crypto

A standard German Steuerberater understands employee income, business income, real estate

and dividends. Give them a wallet export file, a Uniswap transaction history, or a list of staking

rewards, and most of them will either estimate conservatively (which means high taxes) or refuse

to engage with it at all.

What to Look for in a Crypto Steuerberater

- Crypto specialisation listed on their website

If it’s not on the front page, ask explicitly whether they handle DeFi and on-chain transactions.

- Experience defending audits, not just filing returns

Filing is the easy part. If you get audited, you need someone who knows how the Finanzamt

processes crypto cases.

- Proficiency with tax software

They should actively use Koinly, Accointing, or a similar tool. If they want you to manually transfer

everything into a spreadsheet, find someone else.

- Flat fee pricing

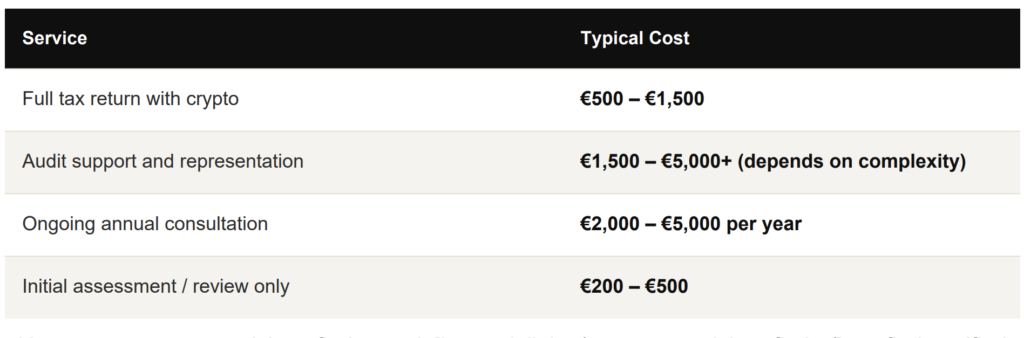

Flat fees of €500–800 for a full crypto return review are common and appropriate. Be wary of

hourly rates with no estimate — crypto cases can get complex quickly.

- DeFi and NFT experience

These are the areas most advisors struggle with. Ask specifically about their experience with

liquidity pools and yield farming.

Expected Costs

14. FAQ — Everything Else You’re Wondering About

Q. Do I have to report small amounts of crypto in Germany?

A. Yes. There is no minimum reporting threshold. All crypto holdings and transactions must be

declared. However, if your total short-term gains for the year are below €600 (the Freigrenze), no

tax is actually owed on those short-term gains. Report everything, pay based on what’s taxable.

Q. Is crypto completely tax-free in Germany after one year?

Yes, for private investors. Gains from cryptocurrency held for more than 12 months are 100%

tax-free under §23 Abs. 1 Nr. 2 EStG, with no upper limit on the gain amount. This is one of the

most generous long-term crypto tax rules in Europe. The exemption does not apply to staking

rewards, mining income, or DeFi yields.

Can the Finanzamt access my exchange data without my consent?

Yes. BaFin regulations require exchanges operating in Germany to share transaction data with the

Finanzamt on request. This includes Kraken, Binance, Coinbase and others. Your trades on these

platforms are not private from the tax authority.

Can I deduct crypto trading losses in Germany?

Yes, within the same tax category. Short-term trading losses can offset short-term trading gains in

the same year, and carry forward to future years. Losses from trading cannot offset staking income

or mining income — those are separate tax buckets. There is no time limit on carrying forward

speculative losses.

Is DeFi taxable in Germany?

Yes, comprehensively. Every DeFi interaction — swaps, liquidity pool deposits, yield harvests,

withdrawals — is a taxable event. The Finanzamt has stated clearly that DeFi is not a grey area. All

on-chain transactions are traceable.

What if I got airdropped tokens in Germany?

Airdropped tokens are taxed as ordinary income on the day you receive them, at the EUR value on

that date. The cost basis for future sales is that receipt-date value.

What if I lost access to my crypto through a hack or lost keys?

You can claim a loss, but you need to document it: original cost, the date you determined the loss

was permanent, and evidence that you no longer have access. The loss is deductible only in the

year you determined it was unrecoverable. You cannot retroactively claim losses in prior years.

How do I report crypto if I’m self-employed in Germany?

Self-employed individuals report crypto activity on Anlage S (self-employment income) or Anlage

EÜR if you use simplified accounting. If trading is your primary income activity, you may need to

register a business (Gewerbe) and pay trade tax.

What’s the penalty for not reporting crypto in Germany?

The Finanzamt can go back 10 years for unreported income. Penalties include late payment

interest at 1.8% per year, negligence penalties of 5–10% of the tax shortfall, and evasion penalties

of 50–100% (plus possible criminal prosecution) for deliberate concealment.

Are there any legitimate tax breaks for crypto in Germany?

Yes: the one-year tax-free holding period (the most powerful), the €600 Freigrenze for short-term

gains, indefinite carryforward of speculative losses, and business expense deductions if you’re

operating as a crypto business. These are the main ones.

How does FIFO work for crypto in Germany?

FIFO (First In, First Out) means the coins you bought first are treated as the first ones sold. This

matters for calculating your holding period and cost basis, particularly when you’ve made multiple

purchases of the same asset at different prices. Consistent method application across your return

is important.

What if my partner or spouse has unreported crypto?

Each person files individually. You are not automatically liable for your partner’s tax. However, if

you filed joint returns (Zusammenveranlagung) and their income was omitted, there could be joint

liability for penalties. Consult a Steuerberater for your specific situation.

DISCLAIMER

This article is based on personal experience and publicly available information about German tax law as of May 2026. It is

not legal or financial advice. German crypto tax rules change frequently — the Bundesfinanzministerium issues new

guidance, the Bundesfinanzhof makes new rulings, and BaFin updates its regulatory requirements on an ongoing basis.

The rules described here are accurate to the best of our knowledge as of the publication date, but must be verified with a

qualified professional before you make any decisions about your crypto holdings, trades or tax filing. Always consult a

Steuerberater who specialises in cryptocurrency. Do not rely solely on any online article, including this one.

Sources: §23 EStG (gesetze-im-internet.de) | Bundesministerium der Finanzen (BMF-Schreiben, 2022) | Bundesfinanzhof

rulings on cryptocurrency | BaFin crypto exchange guidance (2023–2024) | Bundesverfassungsgericht ruling on interest

rates (2021) | Koinly German tax guide | Accointing Germany guide.